Traders have develop into too complacent about black swan dangers.

In case you really feel like housing costs are uncontrolled, you’re not alone.

A Pew Analysis survey carried out in 2021 discovered that half of Individuals now contemplate the dearth of inexpensive housing as a “main” drawback, up from 39% in 2017. (Solely 14% of Individuals assume it’s not an issue in any respect).

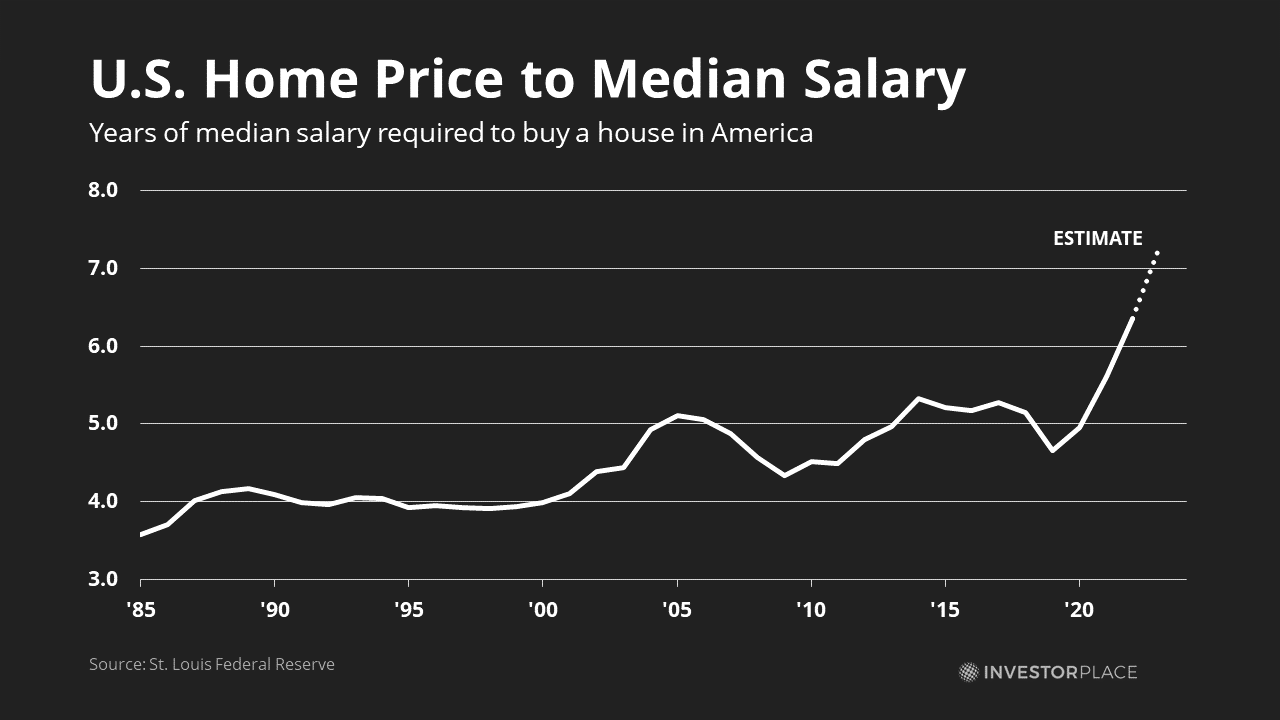

Since then, housing prices have continued to rise. The Nationwide Affiliation of Realtors now estimates that house costs will bounce one other 11% this 12 months, outpacing wage development by a 2x margin. The typical U.S. house may quickly be value 7.5 years of median wage, up from 3.5 years in 1984.

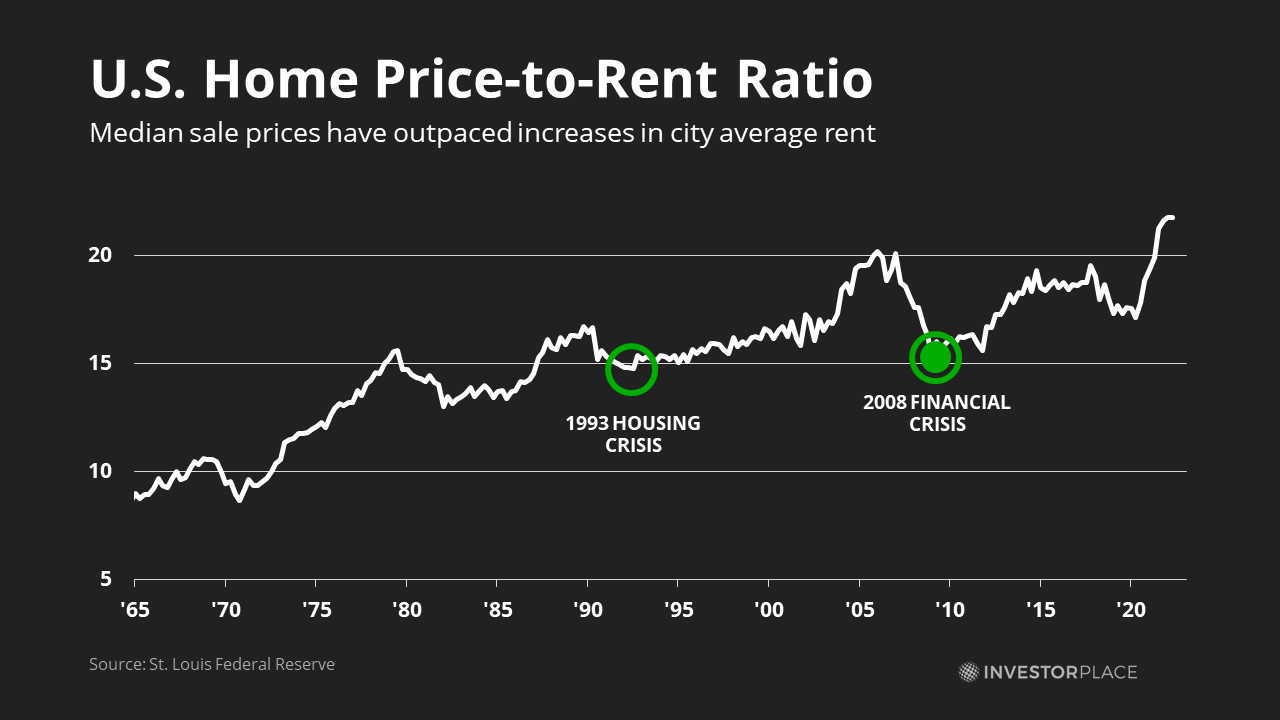

These issues have stemmed from excessive house costs, reasonably than stagnant wages. The worth-to-rent ratio of the typical American house now sits at 21x, nearly 3 times larger than in 1963. Deducting typical bills and upkeep, residential cap charges now sit under 4% for the primary time in fashionable U.S. historical past, in keeping with information from Cornerstone Analysis and CBRE. Cap charges are the anticipated fee of return on an actual property funding, generally calculated as its web working earnings (NOI) to acquisition value.

Excessive costs and declining demand have despatched chills by way of the homebuilding trade – a bellwether for the U.S. actual property market.

“Many potential consumers have paused and moved to the sidelines amid larger mortgage charges, together with ongoing inflation and a variety of macroeconomic and geopolitical considerations,” warned KB Residence (NYSE:KBH) CEO Jeffrey Mezger in a latest earnings name.

The homebuilding agency would submit steerage of $2 billion income, $350 million decrease than Road estimates. Shares of KB Residence have now misplaced 37% 12 months so far.

Actual property analyst Ivy Zelman of Zelman & Associates now predicts a 9% drop in house costs by 2024. A decline to extra historic pricing may see a 20% fall or extra in actual phrases, a future I can foresee taking place over the subsequent a number of years.

Fintech’s Actual Property Downside

These considerations, nevertheless, have been largely ignored by a brand new era of actual property fintech companies. Many of those corporations have solely come public up to now a number of years; companies like insurtech Lemonade (NYSE:LMND) have by no means seen a monetary disaster earlier than. Others have solely lately expanded into riskier parts of actual property. Very like banks in 2008, these unregulated fintechs might be sitting on time-bombs with out ever realizing it.

Nowhere is that this clearer than at Rocket Mortgage (NYSE:RKT), an internet fintech that eclipsed Wells Fargo (NYSE:WFC) in 2018 as America’s largest mortgage author.

In 2020, the Detroit-based fintech generated $16 billion in revenues and $9.Four billion in income from a surge in mortgage refinancing. When a house owner’s mortgage runs at 5%, she or he may gladly pay $20,000 to an organization like Rocket Mortgage to refinance to a 2.5% fee.

Refinancings have was a windfall for Rocket Mortgage, which has used proceeds to load up on mortgages and their servicing rights (MSRs). On the finish of 2021, RKT held $19 billion of mortgages on its books.

In good instances, these methods increase company backside traces. Rocket Mortgage’s web earnings in 2021 was seven instances larger than in 2018. Servicing payment earnings generated $1.Three billion in revenues that 12 months.

However when the tide goes again out, it all of the sudden turns into clear why a financial institution like Wells Fargo was keen to cede floor so simply.

With demand for mortgage refinancings projected to break down, analysts now anticipate Rocket’s web earnings to fall 98% to $214 million in 2022. Even worse, the $19 billion of mortgages on Rocket’s books may shortly develop into a powder-keg of dangerous belongings if debtors start to default.

Within the 2008 monetary disaster, excessive banking leverage meant that the 15% decline in house costs magnified into far higher losses. Lehman Brothers’ 31x debt-to-equity ratio meant {that a} $2.eight billion loss was sufficient to set off its full downfall. Rocket’s 48x debt-to-equity ratio at present signifies that a 2% lower in belongings is sufficient to wipe out its complete fairness base.

No outsider will ever know for certain whether or not Rocket Mortgage’s steadiness sheet is as high-quality as administration claims. However given finance’s lengthy historical past of spectacular leverage and collapses, buyers ought to tread fastidiously to keep away from a repeat of historical past.

Leverage + Actual Property = Powder Keg

Fintech’s actual property leverage drawback extends to iBuyers, corporations that purchase properties with the aim of flipping them for revenue.

In November 2021, Zillow (NASDAQ:Z) introduced it was exiting its iBuying enterprise after dropping over $1 billion in lower than 4 years. And Redfin (NASDAQ:RDFN) has additionally backtracked from the enterprise.

These companies failed regardless of concentrating on extra homogenous housing markets like Phoenix. The “lemon” drawback would have been even worse had they tried to make sight-unseen, all-cash gives in Boston or one other metropolis with much less uniform housing.

But, two actual property companies have continued to threat investor cash: Opendoor Applied sciences (NASDAQ:OPEN) and Offerpad Options (NYSE:OPAD). Collectively, these two iBuying companies carry $11.6 billion in belongings and $9.zero billion in liabilities, giving a mean debt-to-equity ratio of three.5x.

Ordinarily, buyers wouldn’t fear about barely elevated ranges of debt. The typical debt-to-equity ratio within the S&P 500 sometimes ranges within the 2.0x – 2.5x vary, and blue-chip shares like Gartner (NYSE:IT) and Amgen (NASDAQ:AMGN) can comfortably handle ratios of 5x or larger. These companies can use sturdy money flows to cowl curiosity funds ten instances over.

However actual property corporations usually require decrease leverage due to their lumpier earnings. In the present day, the median U.S. actual property funding belief carries solely 1x leverage, in keeping with information from Thomson Reuters. And solely 9 of the 167 American-listed REITs have D/E ratios larger than Opendoor and Offerpad Options.

In the meantime, Opendoor has already began warning buyers that it may lose as a lot as $175 million in adjusted EBITDA this quarter. Add in curiosity and depreciation expenses, and the agency may knock out over 15% of its fairness worth in a single quarter.

And residential costs haven’t even fallen far but.

If house costs fall 20% as the info suggests, Opendoor and Offerpad may shortly fall right into a money crunch. Within the worst-case state of affairs, buyers may see each companies go bankrupt inside months.

The Risks of a Rising Tide

The 12-year bull market has created a way of complacency amongst youthful actual property companies. On Aug. 3, CEO Glenn Sanford of actual property brokerage agency eXp World Holdings (NASDAQ:EXPI) introduced report earnings.

“Throughout the second quarter, eXp continued to extend its market share and income to report ranges, reinforcing that our mannequin was constructed for all market situations and that our agent worth proposition resonates around the globe,” stated Mr. Sanford.

Such claims are untested. The actual property brokerage was launched in October 2009, months after the underside of the monetary disaster. And its multi-level-marketing fashion of splitting commissions with recruiters is untested in bear markets.

I’ve warned buyers earlier than in regards to the dangers of shopping for fintechs centered on conventional, cut-throat enterprise.

“Although LMND has a elaborate front-end web site, its rear nonetheless seems to be like a P&C store…

Lemonade will comply with an analogous all-or-nothing path to profitability. Both the corporate will develop into the subsequent Geico (value $50 billion or extra) or it can blow up like so many different P&C insurers earlier than it over mispriced threat.”

Since then, shares of Lemonade have misplaced 67% of their worth.

However even these losses may pale compared to what Rocket, Opendoor and Offerpad may face if declining actual property values blow up their steadiness sheets. Extremely leveraged companies are all the time enjoying with fireplace. This time, falling actual property costs might be the spark that turns into an inferno.

Revealed First on InvestorPlace. Learn Right here.

Featured Picture Credit score: Photograph by Kindel Media; Pexels; Thanks!

The submit Warning! A Housing Market Crash Will Tank These Three Shares. appeared first on ReadWrite.