Cash is one in every of humankind’s most outstanding improvements. It makes it attainable to commerce services throughout nice geographic distances, between individuals who could not know one another and don’t have any explicit motive to belief one another. It could even be used to switch wealth and assets over time. With out cash, commerce and commerce—all human financial exercise, actually—can be severely constrained when it comes to time and area.

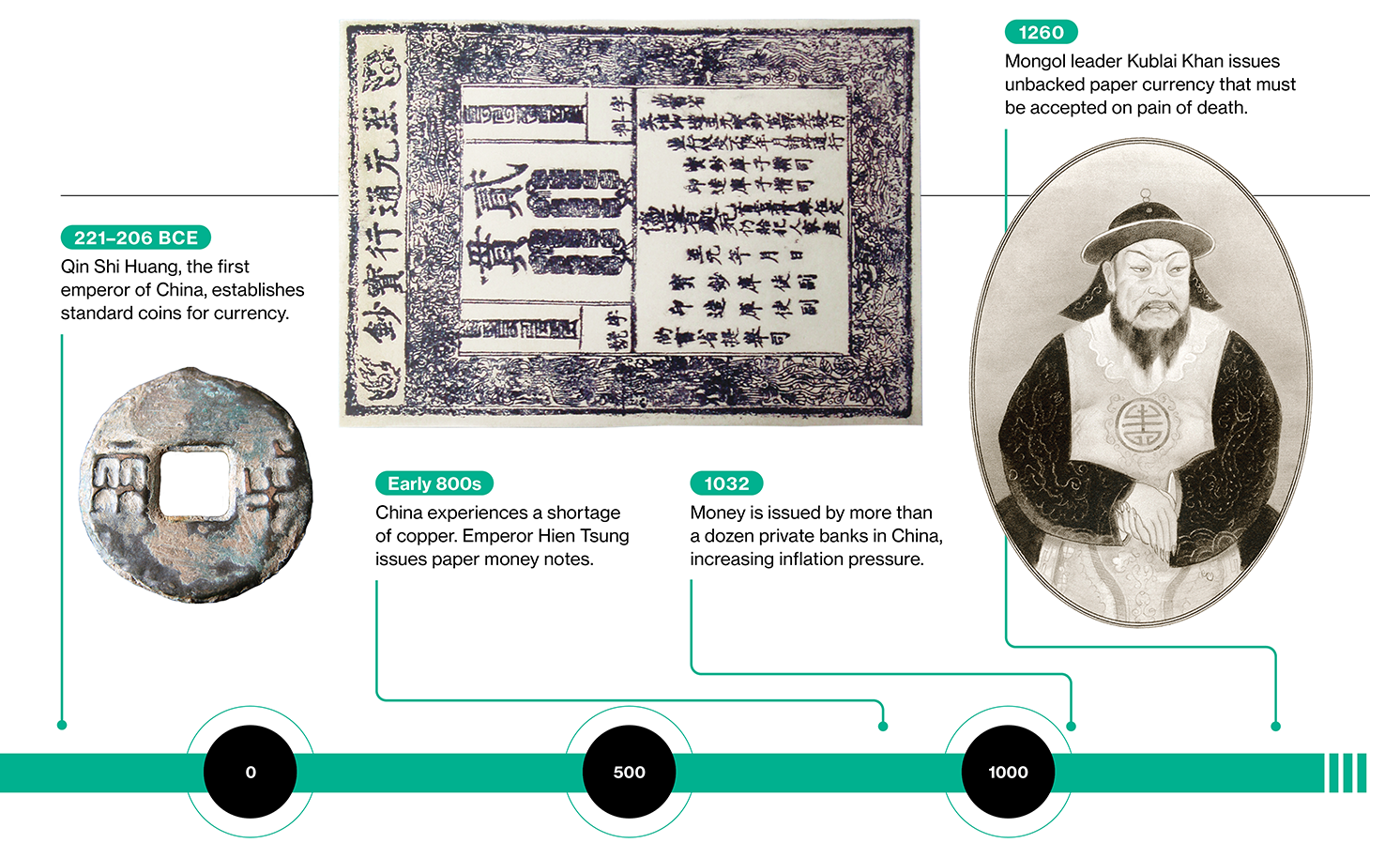

The privilege of issuing cash is synonymous with financial energy. So it ought to come as little shock that historical past is replete with examples of foreign money competitors, each inside nations and between them. In China, dwelling of the world’s first paper cash, currencies issued by non-public retailers and provincial governments competed for a lot of centuries. Certainly, banknotes issued by governmental and personal banks coexisted in China as late as the primary half of the 20th century.

What lastly, decisively ended this competitors was the emergence of central banks, which got the unique privilege of issuing authorized foreign money and tasked with sustaining its stability. This shift occurred fairly early in Sweden; the world’s oldest central financial institution, the Riksbank, was established there within the 17th century. In China, competitors closed with the founding of the Folks’s Financial institution of China in 1948, shortly earlier than the formal creation of the Folks’s Republic of China. For the reason that central banks stepped in, competitors has been largely worldwide, with the relative worth of currencies relying on the popularity and stability of the central banks issuing them.

We now stand on the threshold of one other period of upheaval. Money is on the best way out, and the digital applied sciences which can be changing it may remodel the very nature and capabilities of cash. Immediately, central-bank cash serves without delay as a unit of account, a medium of change, and a retailer of worth. However digital applied sciences could lead on these capabilities to separate as sure types of non-public digital cash, together with some cryptocurrencies, achieve traction. That shift may weaken the dominance of central-bank cash and set off one other wave of foreign money competitors, one that would have lasting penalties for a lot of nations—significantly these with smaller economies.

In historical societies, objects such asshells, beads, and stones served as cash. The primary paper foreign money appeared in China within the seventh century, within the type of certificates of deposit issued by respected retailers, who backed the notes’ worth with shops of commodities or valuable metals. Within the 13th century, Kublai Khan launched the world’s first unbacked paper foreign money. His kingdom’s payments had worth just because Kublai decreed that everybody in his area needed to settle for them for cost on ache of demise.

Kublai’s successors had been much less disciplined than he was in controlling the discharge of paper foreign money. Subsequent governments in China and elsewhere gave in to the temptation of printing cash recklessly to finance authorities expenditures. Such wantonness sometimes results in surges of inflation and even hyperinflation, which in impact quantities to a precipitous fall within the amount of products and companies {that a} given sum of cash can purchase. This precept is related even in fashionable instances. Immediately, it’s belief in a central financial institution that ensures the widespread acceptance of its notes, however this belief should be maintained via disciplined authorities insurance policies.

To many, nevertheless, money now appears largely anachronistic. Actually dealing with bodily cash has turn out to be much less and fewer widespread as our smartphones permit us to make funds simply. The way in which through which folks in rich nations like the USA and Sweden, in addition to inhabitants of poorer nations like India and Kenya, pay for even primary purchases has modified in only a few years. This shift could seem like a possible driver of inequality: if money disappears, one imagines, that would disenfranchise the aged, the poor, and others at a technological drawback. In observe, although, cell telephones are practically at saturation in lots of nations. And digital cash, if carried out accurately, could possibly be a giant drive of monetary inclusion for households with little entry to formal banking techniques.

Money nonetheless has some life in it. Throughout the covid pandemic, at the same time as contactless funds turned extra prevalent, the demand for money surged in main economies together with the US, presumably as a result of folks seen it as a secure type of financial savings. Many states within the US have legal guidelines in place to guarantee that money is accepted as a type of cost, one thing that might shield individuals who can’t or don’t wish to pay via different means. However shoppers, companies, and governments have usually welcomed the shift to digital types of cost, particularly as new applied sciences have made them cheaper and extra handy.

The decline of bodily money, as soon as valued as probably the most definitive type of cash, is however a small function of the quickly altering monetary panorama, although. Probably the most dramatic forces of change has been the rise of cryptocurrencies, which have shaken long-held precepts about cash and finance.

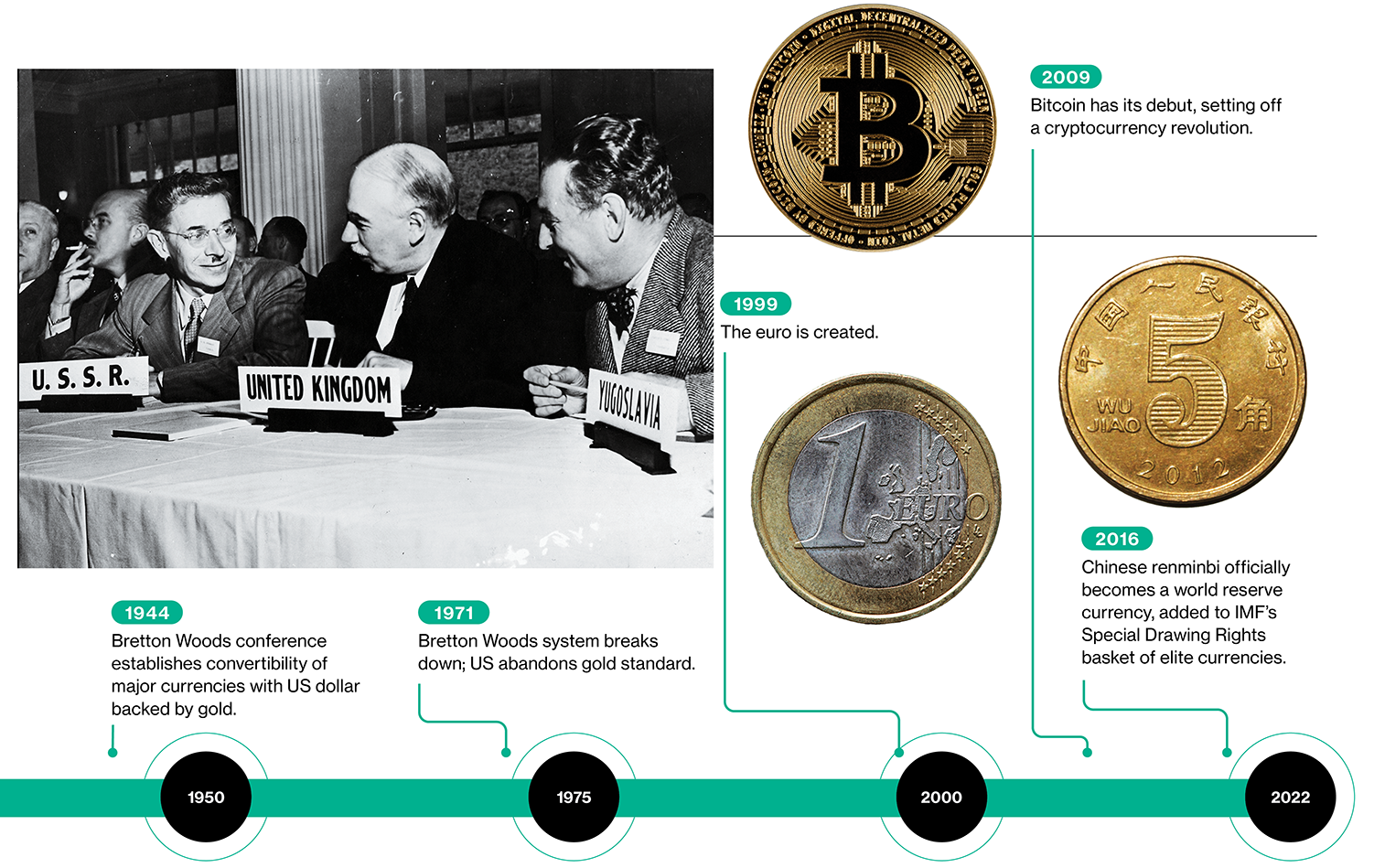

Bitcoin, the cryptocurrency that began all of it, could not have a lot of a job to play on this financial future.

Bitcoin was designed to allow folks to finish transactions pseudonymously (utilizing solely digital identities relatively than actual ones) and with out the intervention of a trusted third social gathering resembling a central financial institution or monetary establishment. In different phrases, anybody with a pc may conduct transactions—no bank card or checking account essential. Cash are issued and transactions validated via a pc algorithm that runs autonomously; the id of its creator stays unknown to at the present time.

The timing of Bitcoin’s introduction in early 2009, when the worldwide monetary disaster had decimated belief in governments and banks, couldn’t have been higher. However even because it gained in reputation, Bitcoin stumbled in its primary makes use of. The volatility of Bitcoin’s worth, with wild worth swings from in the future to the following, has made it an unreliable methodology of cost. Furthermore, it seems that the cryptocurrency doesn’t assure anonymity—customers’ digital identities can, with some effort, be linked to their actual identities (in some methods it is a good factor, as Bitcoin transactions that after fueled the darkish internet, the place unsavory and illicit commerce is carried out, have fallen sharply). Immediately, Bitcoin and different cryptocurrencies prefer it have largely turn out to be speculative monetary belongings, with little intrinsic value and sky-high valuations that aren’t backed by something apart from traders’ religion.

A brand new technology of cryptocurrencies is rising that guarantees to repair a lot of Bitcoin’s flaws. Stablecoins, cryptocurrencies whose secure worth comes from being backed by reserves of US {dollars} or different respected fiat currencies, are proliferating. Stablecoins are billed as dependable, simply accessible digital cost techniques that may make each home and worldwide funds cheaper and faster. Nonetheless, not like Bitcoin, which is absolutely decentralized, they require transactions to be validated by the issuing establishment—which could possibly be a financial institution, an organization, or simply a web based entity. This implies customers should belief that establishment to validate solely reputable transactions and maintain sufficient reserves, and regulators at the moment don’t require impartial verification of both of these actions. Thus, regardless of their laudable purpose of assembly the demand for higher cost techniques, stablecoins have raised a raft of issues.

Even with all these rising pains, the cryptocurrency revolution has expanded the frontiers of digital cost applied sciences and helped mild a fireplace underneath central banks. Lengthy seen as conservative establishments proof against main change, many are actually coming into the digital race.

Confronted with the rising irrelevance of their paper currencies, many central banks world wide need to concern their cash in digital kind. Main economies resembling China, Japan, and Sweden are experimenting with central-financial institution digital currencies (CBDCs), which in impact are simply digital variations of the currencies they now concern as notes and cash. The Bahamas and Nigeria have already rolled out their CBDCs nationwide. International locations together with Brazil, India, and Russia are within the strategy of initiating their very own experiments.

Some nations see CBDCs as a strategy to broaden entry to the formal monetary system—even households with out financial institution accounts or bank cards would achieve entry to a secure and cheap digital cost system. Different nations are pursuing CBDCs to extend the effectivity and stability of digital cost techniques. Sweden’s e-krona is being pitched as a backstop in case the cost system managed by private-sector firms, which could work completely effectively underneath most circumstances, ought to fail due to both technical issues or confidence points.

CBDCs may additionally assist preserve the relevance of central-bank retail cash in nations the place digital funds have gotten the norm. China, for instance, is pursuing its digital renminbi at a time when two monetary titans, Alipay and WeChat Pay, are striving to dominate the cost panorama.

CBDCs have many different benefits, too. They may deliver sure forms of financial exercise out of the shadows and into the tax web (not like money transactions, which frequently go unreported to tax authorities), scale back counterfeiting, and make it more durable to make use of official cash for illicit functions resembling cash laundering, drug trafficking, and financing of terrorism. However they might threaten no matter minimal vestiges of privateness we nonetheless take pleasure in—in spite of everything, all the pieces digital leaves a hint. Transactions utilizing CBDCs are more likely to be auditable and traceable, as no central financial institution would wish to permit its cash for use for illicit transactions.

What is going to the world of cash seem like in 5 or 10 years’ time? We may envision a world the place many individuals maintain digital wallets with a mixture of cash in conventional financial institution accounts, stablecoins managed by non-public firms, and maybe a number of CBDCs, transferring them round relying on world situations. Then once more, nobody is aware of how effectively stablecoins and CBDCs will coexist. Meta (previously Fb), for instance, had deliberate to roll out its personal stablecoin. However the venture was quashed by US regulators, who had been involved about Meta’s goals and in regards to the chance that the stablecoin could possibly be used to finance illicit transactions inside and throughout nationwide borders.

The essential case for stablecoins as extra environment friendly and simply accessible types of digital cost could possibly be undercut by CBDCs. For the second, stablecoins appear to be holding their very own—there have been greater than 30 in circulation as of March 2022, with a complete worth of about $185 billion. And there may be the chance that stablecoins constructed on high of large-scale industrial ecosystems resembling Amazon’s may achieve vital traction as technique of cost.At any fee, insofar as their stability is determined by their being backed by fiat currencies, stablecoins are unlikely to turn out to be impartial shops of worth. In different phrases, they’d be used primarily as a result of they’d be cheaper or extra handy technique of cost.

Nonetheless it performs out, the digital-foreign money revolution goes to have implications for the worldwide financial system. Take cross-border funds, that are inherently sophisticated as a result of they contain a number of currencies, establishments utilizing totally different technological protocols, and ranging units of laws. All this makes worldwide funds gradual, costly, and troublesome to trace in actual time. Cryptocurrencies, which could be shared freely throughout borders, will scale back these impediments, enabling practically instantaneous cost and settlement. Even CBDCs may ease the frictions if they’re made out there to be used internationally and achieve widespread acceptance.

Extra-efficient worldwide cost techniques will deliver a number of advantages. For one factor, they may make it simpler and cheaper for financial migrants to ship remittances again to their dwelling nations—a course of that at the moment prices a mean of 6% of the transaction quantity, in keeping with the World Financial institution. The estimated prices are even greater for remittances going to low-income nations, a lot of which rely upon such inflows for a big share of nationwide earnings.

In precept, monetary capital will be capable to stream extra simply inside and throughout nations to the best funding alternatives, elevating world financial welfare—a minimum of as measured by GDP and consumption capability. However simpler capital flows throughout nationwide borders may also pose dangers for a lot of nations, making it a lot more durable to handle their change charges and their economies.

The ensuing challenges can be particularly thorny for smaller and fewer developed nations.

Nationwide currencies issued by their central banks, significantly these currencies seen as much less handy to make use of or extra risky in worth, could possibly be displaced by non-public stablecoins and maybe additionally by CBDCs issued by the main economies. This could end in a lack of financial sovereignty: much less outstanding central banks would lose management over the circulation of cash of their economies. The phenomenon of “dollarization,” whereby a trusted overseas foreign money supplants a risky home foreign money (lengthy the bane of many Latin American nations), could possibly be intensified by the proliferation of digital currencies. In locations resembling Iran and Turkey, now we have already seen folks use cryptocurrencies to get round restrictions on capital outflows when currencies had been plunging in worth, enabling them to spirit funds out of their nations and into safer investments overseas.

Even for the main reserve currencies, there are some shifts in retailer, although the long-standing dream of many governments world wide—knocking the US greenback off its pedestal because the dominant world reserve foreign money—will in all probability stay simply that for the foreseeable future. Certainly, it’s possible that stablecoins backed by the greenback will achieve widespread acceptance relative to stablecoins backed by different currencies, not directly rising its relative prominence. However the digital renminbi is poised to realize traction as a way of cost, and even a gradual and modest improve within the renminbi’s use, together with an increase in stablecoins, may scale back the significance of different reserve currencies, together with the euro, the British pound sterling, the Japanese yen, and the Swiss franc.

In terms of cash’s operate as a medium of change, we are able to count on extra competitors between non-public and fiat currencies. In precept, this could result in funds which can be cheaper and faster—benefiting shoppers and companies—whereas additionally motivating issuers, whether or not non-public or official, to train self-discipline so as to protect the worth of their currencies.

To help MIT Expertise Evaluate’s journalism, please contemplate turning into a subscriber.

However it’s value conserving in thoughts that know-how can have unpredictable penalties. Moderately than resulting in a proliferation of personal and official currencies that compete on a degree enjoying area, the digitization of currencies may make financial energy much more concentrated. If main currencies such because the greenback, the euro, and the renminbi are simply out there worldwide in digital kind, they may displace the currencies of smaller and fewer highly effective nations. Digital currencies issued by giant companies, profiting from the businesses’ already dominant industrial or social media ecosystems, may achieve traction too. Except they’re quashed by governments, they might in the future flip into impartial shops of worth by giving up their fiat-foreign money backing. This might create much more financial instability if particular person nations wound up having a number of issuers of cash, with competing home currencies fluctuating in worth relative to at least one one other.

All that’s sure is that the worldwide financial system is on the brink of momentous change wrought by the digital revolution. It stays to be seen whether or not this in the end advantages humanity at giant—or exacerbates current home and world inequities.

Eswar Prasad is a professor within the Dyson Faculty at Cornell College, a senior fellow on the Brookings Establishment, and creator of The Way forward for Cash: How the Digital Revolution Is Remodeling Currencies and Finance.